AppFolio (APPF) - SHORT

My investment thesis

Company Background

AppFolio (APPF) is one of the leading providers of software solutions for residential real estate property managers. The AppFolio platform provides several useful tools that property mangers can use to better run their operations, including a resident portal (for filing maintenance requests, communicating with other neighbors, making online rent payments, etc.), accounting and reporting systems, operational insights (e.g. tracking vacancies and payment delinquencies), and marketing/leasing services (e.g. listing apartment openings, tenant screening). In short, AppFolio acts as the manager’s system of record, helping digitize real estate property management workflows. As of 3Q22 the company counted over 18k property manager customers who collectively oversee 7.1m units (mostly multifamily apartments). AppFolio historically has targeted SMB managers (with 50-500 units) but has begun shifting its focus upmarket (mid-market and corporate). The company was founded in 2006 and went public in 2015. In Sep 2020, AppFolio fully divested its MyCase business, which provided vertical software solutions to the legal industry.

AppFolio charges property managers a base subscription fee per unit. The basic Core offering is $1.50/unit/month and the Plus offering - which is meant for larger customers with more complex portfolios and offers customizable workflows, revenue management tools and better partner integrations - is $3.0/unit/month. These subscription fees account for ~30% of total. In addition, AppFolio offers “Value Added Services” that include online payments (for residents and vendors), tenant screening services (background checks, income verification, rental history), insurance and a few other tools. These VAS are priced on a per use basis, either as percentage of the transaction amount (payments) or a flat fee per use (tenant screening, insurance). VAS accounts for ~70% of revenue.

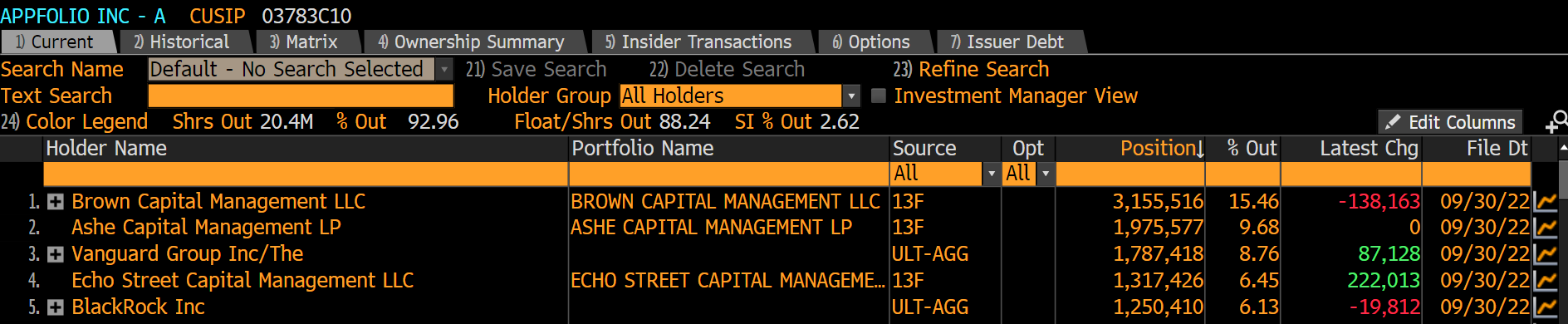

AppFolio is headquartered in Santa Barbara, CA. The company has dual-class structure in which Class A owners have one vote per share and Class B owners (mostly insiders) have 10 votes per share and thus control ~90% of voting rights. The largest shareholder with ~25% ownership (between Class A and B) is Maurice Duca, a successful software entrepreneur and investor (with IGSB) based in Santa Barbara. In the recent 13D filing, Duca indicated he is pushing the Board to “immediately revise its management incentive arrangements to align with, and emphasize, clear profitability growth objectives.” (More on this in later section). Other >5% holders are seen below.

Four keys points

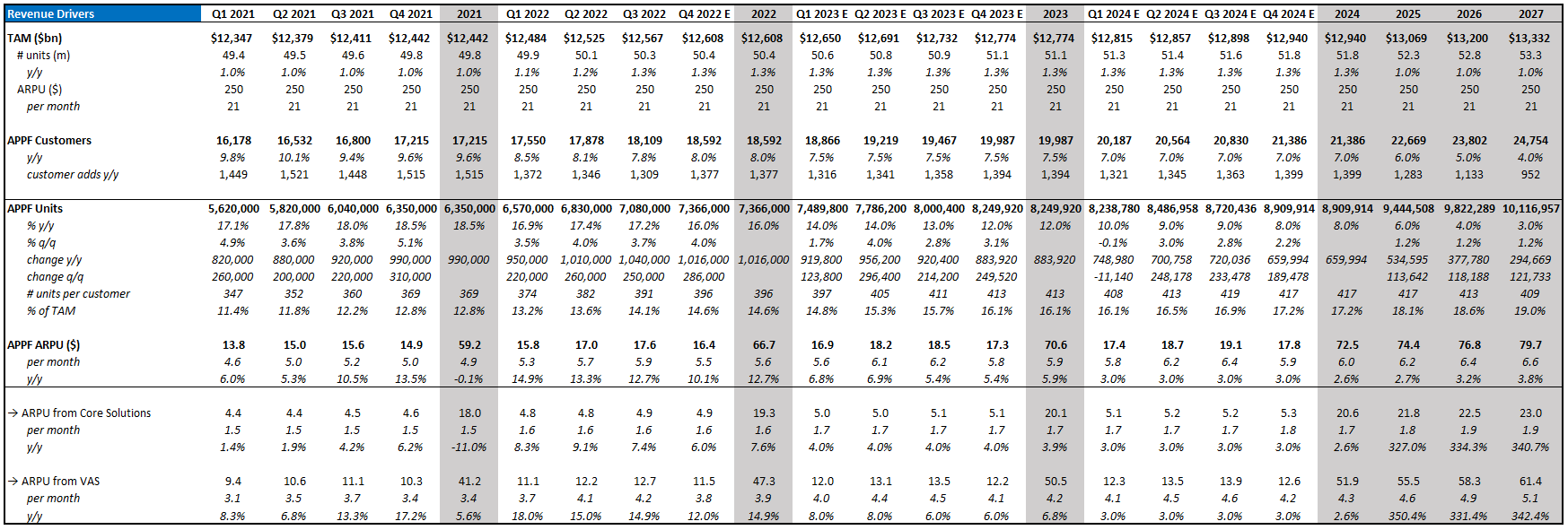

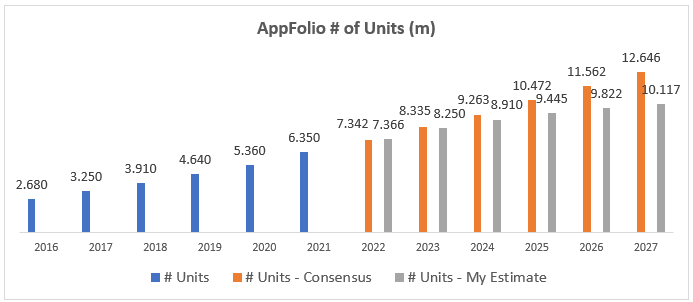

Unit growth likely to slow. APPF has 7.1m units today, up from 4.6m units at end of 2019, a 17% CAGR. This pace of growth is not sustainable as the market for property management software is reaching saturation. There are ~51m residential rental units in the US (single-family and multifamily), plus another 28m community association units (which are a non-core focus area). Between RealPage (20m units), AppFolio (7m), Yardi (8m+ units), and other vendors (including Entrata, ResMan, MRI, and more) it is fair to assume that approximately 50m units (60% of total) are already accounted for. And many of the remaining property managers may not want to pay the cost for an outsourced software vendor. As such, the greenfield opportunity set is shrinking, forcing these companies to get more competitive and fight for customers. We have seen this with AppFolio, which historically focused on SMB customers (property managers with 50-500 units) but in the past 24 months has shifted upmarket to mid-market (500-1500 units) and corporate (1500+ units) segments. However, channel feedback suggests their product is more suited to smaller property managers and lacks the sophistication and ease of integration that larger customers like from peers such as RealPage and Yardi. In addition to AppFolio’s challenge in moving upmarket, their peers are doing the reverse and shifting their own focus on smaller customers, putting some price pressure on APPF.

In short, as the market is becoming more saturated, the vendors are having to think more about competitive displacements and this could be a headwind for AppFolio’s unit growth. AppFolio was adding ~700k units per year from 2018 to 2020 and this jumped to ~1m units per year in 2021/22 as the very strong rental market helped spur demand from managers (who had extra income and needed better systems to manage it all). Consensus estimates show AppFolio reaching 10.5m units by 2025, a 13% CAGR from today, adding ~1m units per year. In my estimates, I see AppFolio unit growth reverting back towards the ~700k per year level, reaching 9.5m by 2025 (9% CAGR) given the headwinds described above.

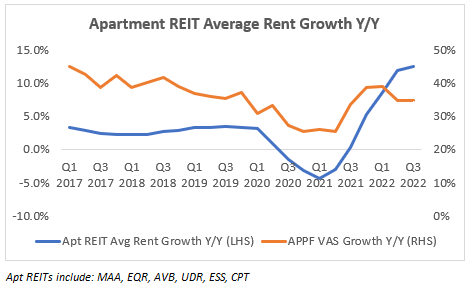

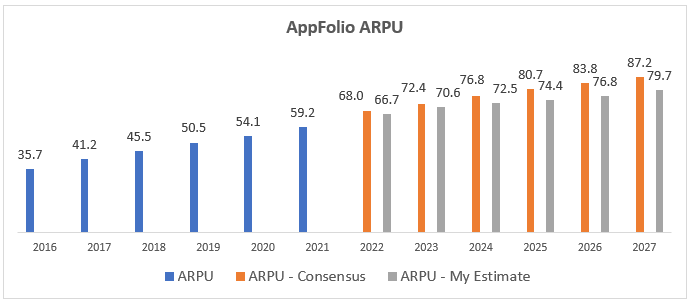

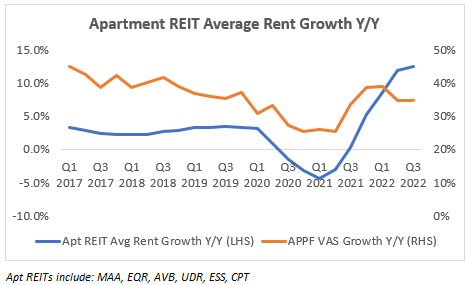

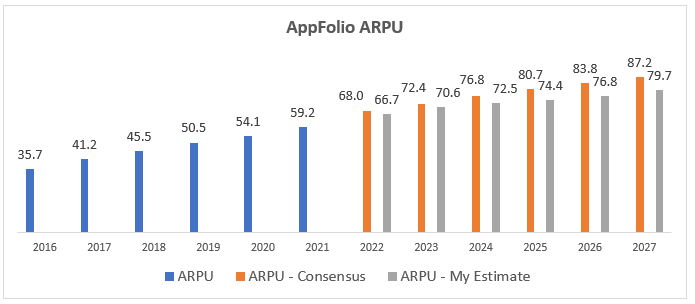

VAS growth will face rent price headwind. VAS accounts for ~70% of AppFolio revenue and management has been clear that they are focused on growing these services to increase revenue per unit to offset the expected deceleration in unit growth. The company doesn’t break out the mix of services, but one former executive suggested payments was 70-80% of VAS revenue and is at 80-90% penetration levels. The payments service enables tenants to pay their rent online via ACH or credit card; APPF collects a small percentage of each transaction (customers pay a 3% processing fee but much of this goes to payment processor/network). This means that payments revenue is directly tied to the level of rent price. Apartment rental prices dipped in 2020 and 2021 but rebounded strongly in 2022 as rental demand returned post-Covid. We can see this impact on APPF VAS growth, which dropped from high-30s to mid-20s at the trough in 2021 before returning back to mid/high 30s today.

The apartment REITs have indicated that 4Q rent growth is decelerating further. Without intending to make an explicit macro call, it seems safe to say that rental growth will not sustain at the high levels of 2021/22 and instead should eventually revert back towards the normalized average of 3-4% p.a. Layering that type of annual rent growth on top of my estimate for unit growth results in my estimate for ARPU (which includes core as well as VAS) coming in below consensus.

Other VAS services - insurance, tenant screening, maintenance call center - are at lower penetration rates and thus can offer a growth offset, but payments is the key driver of VAS growth in the next couple quarters at least.

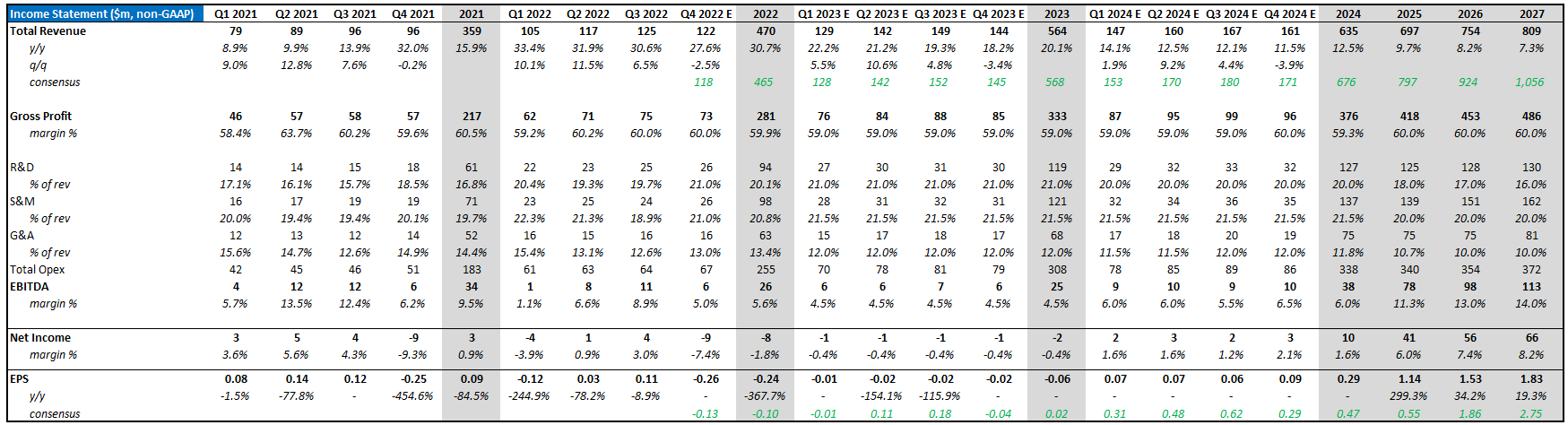

Long-term margin path unclear. APPF gross margin has been consistently at ~60%. Management doesn’t break this out, but based on channel checks we can imply that the core subscription fees carry ~80% gross margins (similar to other SaaS) while VAS revenues carry ~50% gross margins due to the costs paid to third-party providers of those services. APPF was generating low-single-digit operating margin and FCF margin until 2021, when these turned negative, which was attributed to the increased investment (both R&D and S&M) associated with the shift in focus to upmarket customers. Guidance for 2022 points to negative operating margin but slightly positive FCF. The challenge is getting comfortable with the sustainable long-term margin profile that APPF can achieve. It is reasonable to believe that APPF can reach ~20% FCF margins over time (several years at least), which is what peer RealPage achieved for several years before being taken private. I can see this happening if management realizes that the market is reaching saturation and shifts focus from unit growth to ARPU growth.

However, there are two key issues with this: 1) management bonus incentives emphasize unit growth over profitability - 60% of the 2022 cash bonus targets is based on hitting net new units target, while 20% is based on hitting revenue target and just 20% is based on operating margin target; and 2) competitive dynamics may limit ability to expand margins, especially as APPF shifts upmarket, which can introduce price pressure and force the company to continue investing in R&D and S&M above target. Consensus estimates show APPF slowly increasing operating and FCF margin by 200-300bps per year, ultimately reaching 11% by 2027. This feels like an accurate landing spot for APPF as it may struggle to reach the profitability level of its larger peer RealPage.

It is worth noting that at their Analyst Day in October 2022, APPF did not provide any specific margin target or timeline, just a vague plan to reach positive FCF and a comment from the CFO that the “journey [to increase FCF margin to ‘healthy level’]…will take a few years.” One aspect that could spur quicker improvement in profitability is the engagement of Maurice Duca, the largest shareholder (25%, including Class B voting shares) who has stated his intention to push the Board to revise its management incentive program with a focus on profitability objectives. But this will have to be proven over time.

Valuation is expensive. APPF has been a relative outperformer over the past 12 months with the stock down just 8% vs. apartment REITs down 20-30% and QQQ down 28%. APPF currently trades at $114 per share for a market cap of $4bn. It is valued at 7x 2023 sales and 6x 2024 sales (on my estimates), putting APPF amongst the top third of the SaaS universe, which feels overly optimistic given lower gross margin and lower recurring revenue stream.

The best comp for APPF is RealPage, which was acquired by Thoma Bravo in early 2021 for $9.7bn at 7.5x 2021E sales (34x FCF). I apply a heavy discount to that multiple given 1) RealPage was market leader already at scale; 2) APPF has lower margins; 3) market conditions in early 2021 were much more favorable than today. As such I value APPF at 5x 2024 sales, which implies a price of $90 per share (21% downside).

If we look at other vertical SaaS peers, there is a bifurcation between those with high FCF margins (DOCS, VEEV, TYL) - valued at 6-9x 2024 sales - vs. those with low or negative FCF margins (PCOR, NCNO, QTWO, TOST) which are valued at 2-6x 2024x sales. APPF clearly falls into the latter bucket, further supporting my use of 5x.

In a bull case where we apply 7x to 2024 consensus sales (higher than me), the implied price of $133 per share, just 17% upside from current levels. A bear case of 4x my 2024 sales estimate implies a price of $73 (36% downside). This risk/reward is attractive given it seems unlikely the multiple will re-rate higher in the current environment.

Risks to upside

Unit growth remains resilient as APPF is more successful than expected in taking share from up-market competitors

Rent price growth remains higher and, thanks to demographic forces, stabilizes above prior long-term average (3-4%), supporting higher VAS revenues

Management, under new CFO and pushing from large shareholder, provides clearer guidance on path to margin improvement

APPF becomes an acquisition target for PE or others who can run similar playbook to RealPage

Model - Revenue Drivers & Income Statement

See below for my estimates of key drivers of revenue and income statement. Feel free to reach out (twitter @MBFcapital or email mbfcapital5@gmail.com) if you want me to share my model in more detail.